Hawaii 1031 Exchange

We have successfully completed many exchanges, helping our clients defer hundreds of thousands of dollars in taxes.

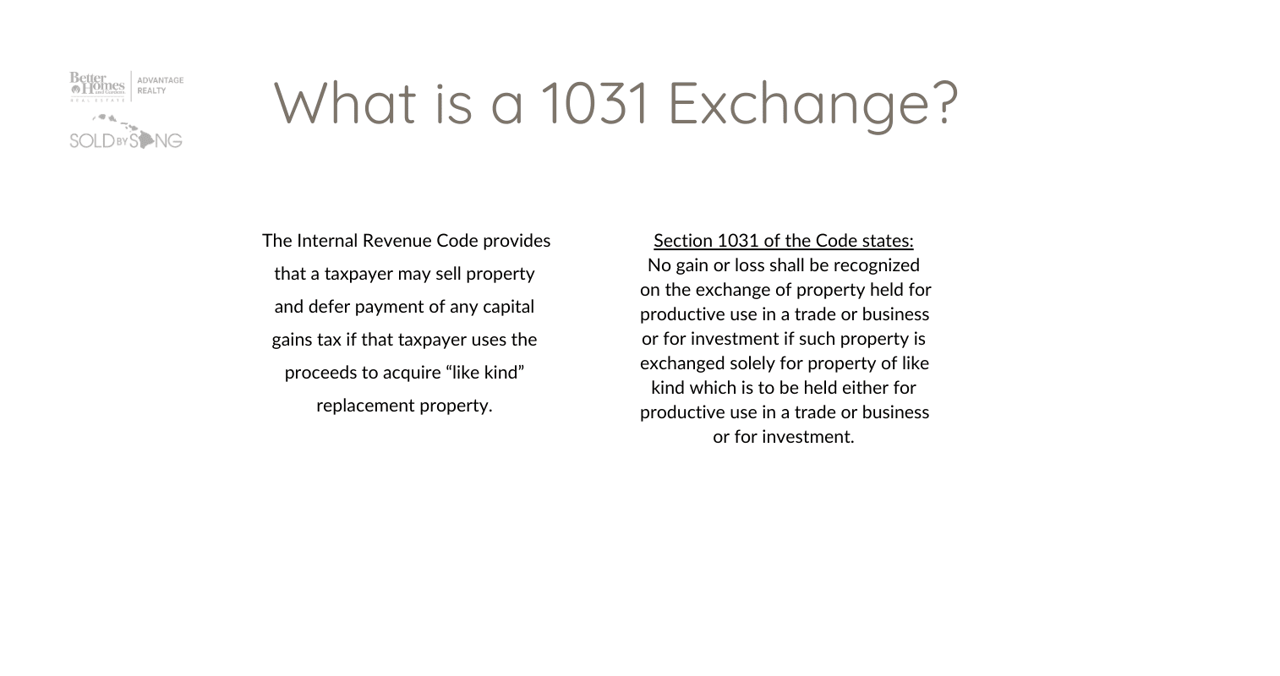

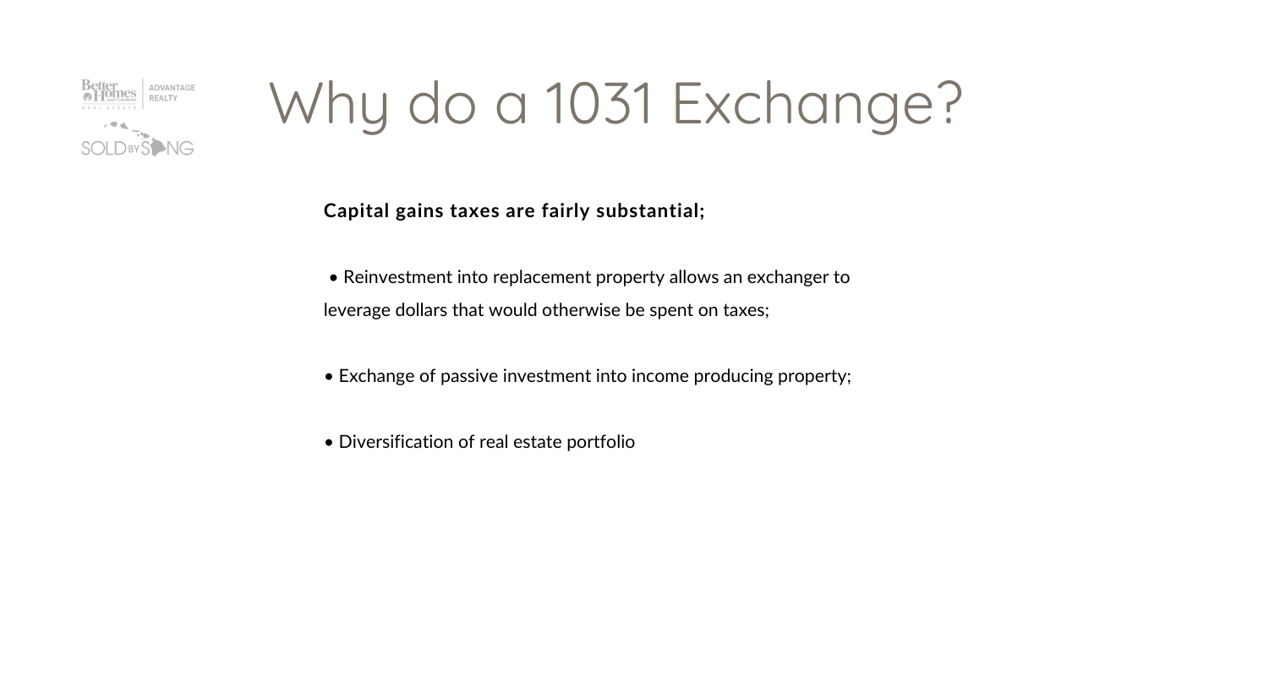

Whenever you sell an investment property and you have a gain, you generally have to pay tax on the gain at the time of sale. Section 1031 of the IRS Tax Code provides an exception and allows you to postpone paying tax on the gain if you reinvest the proceeds into a new investment property as part of a qualifying like-kind exchange. Keep in mind, the deferred gain in a 1031 is tax-deferred, but it is not tax-free.

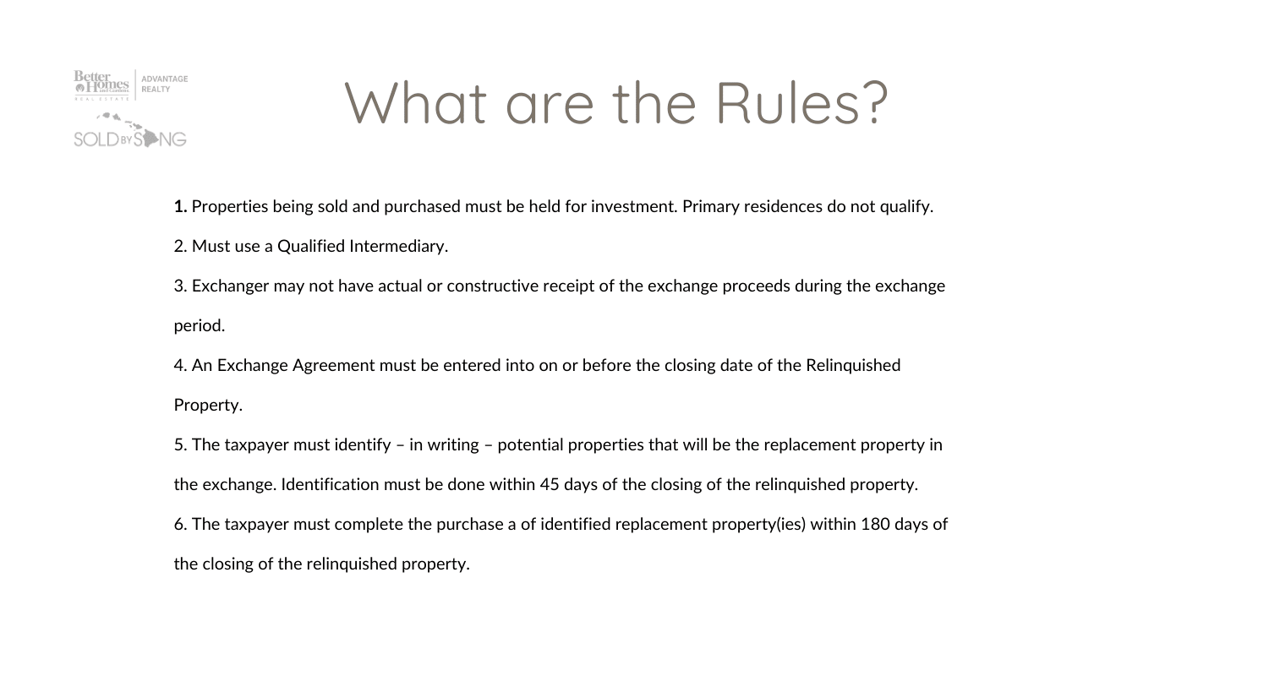

Owners of investment and business property may qualify for a 1031. Individuals, C corporations, S corporations, partnerships (general or limited), limited liability companies, trusts and any other taxpaying entity may set up an exchange of business or investment properties for business or investment properties under Section 1031.

Report on Form 8824 and file it on your tax return for the year in which the exchange occurred.

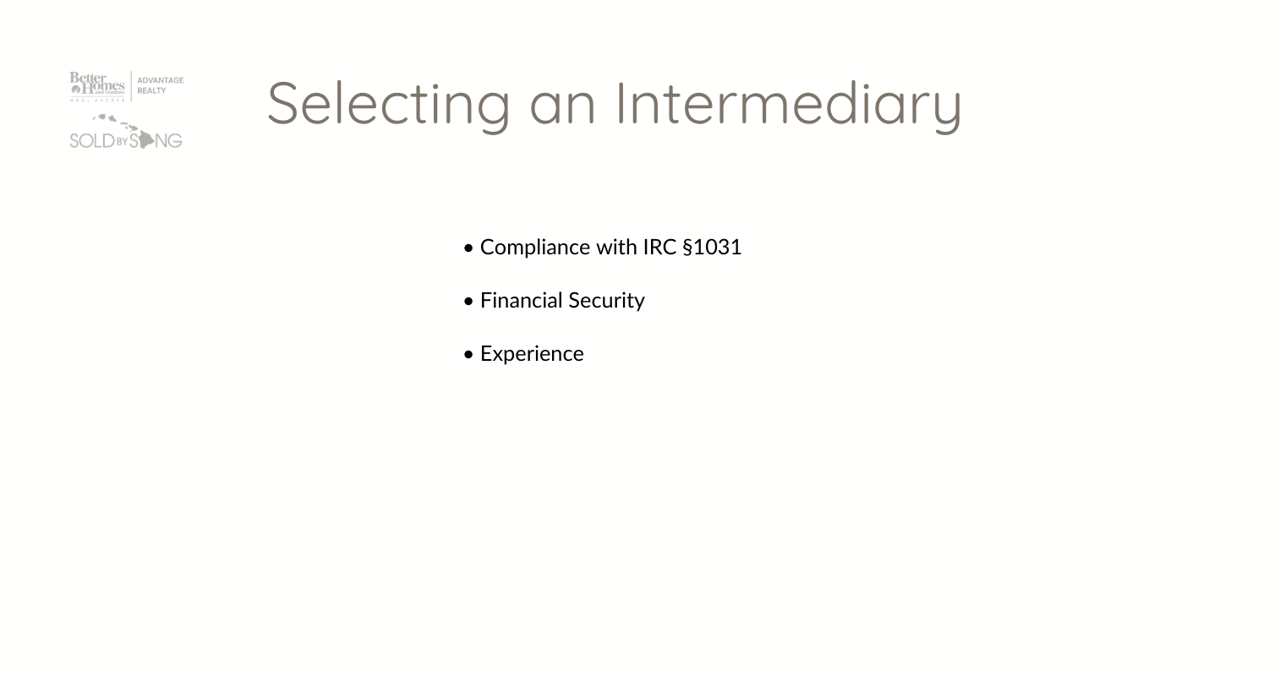

Always consult with your licensed tax professional or tax attorney. Be wary of experts who promote or guarantee tax savings or improper exchanges for nonqualifying properties such as second homes.